Live Music Archive

Live Music Archive Librivox Free Audio

Librivox Free Audio Metropolitan Museum

Metropolitan Museum Cleveland Museum of Art

Cleveland Museum of Art Internet Arcade

Internet Arcade Console Living Room

Console Living Room Books to Borrow

Books to Borrow Open Library

Open Library TV News

TV News Understanding 9/11

Understanding 9/11tv Public Affairs CSPAN December 27, 2012 5:00pm-8:00pm EST

5:00 pm

meanwhile, its gross excesses' remained out of sight. until some believe their own rhetoric -- read ben bernanke -- about moderation. but when the global minotaur was mortally wounded, it left the global economy in disarray. it has put the world in permanent crisis. the minotaur was slain by a brave warrior named theseus. its death ushered a new era of tragedy, history, philosophy. our very own global minotaur died as the victim of wall street bankers. what will its demise bring? should be hope for a new era in which wealth does not require

5:01 pm

poverty? will be develop a system where no longer will abstract power waned while others get stronger? the global minotaur will be remembered as a remarkable piece to whose rain created and destroyed the illusion that the global economy was stable. thank you. [applause] right. questions? i think i am going to moderate myself. ok, you have to line up. this is the way you do it here, isn't it? >> that is a brilliant vision of where we have been. can you elaborate a little bit more on where you see us going?

5:02 pm

>> very briefly, i think that we are in a state of sustained bewilderment. because, let's face it. in the 1930's, the new deal, despite some early successes failed by 1936 or 37. 1938, we have the second great depression. it was only the war that managed to do the recycling the new deal failed to accomplish, due to fdr's backtracking. now we have a world economy which conceivably, that technically finds its way forward to plug the gaps and black holes. 20the g-20 easily agreed to a plan that is very much like that which john maynard keynes

5:03 pm

proposed in 1944. but it is unlikely they will. it is a comedy of errors. the european leaders are competing to produce a plan that is more idiotic. they are so entrenched. they are so parochial. they are beyond squabbles. they have a horizon of 8 months to the next federal election in germany, for instance. greece therefore is the sick person europe. of the world. meanwhile, the united states of america is ungovernable. you have a system in this country that was created to create this country as an ungovernable state. you have congress, the president canceling each other out. how the president -- whoever the president might be -- do anything? you have china -- finding it

5:04 pm

impossible to provide a replacement for the demand that the west has done away with. so, i do not have an answer for your question. bewilderment. >> my question is about consumer demand and the extent to which the old system depended on it. if we do not have it to the same degree, could there possibly be a new economy? i cannot know how to say all of these in the right economic terms. i will say what i am thinking and see what you make out of it. its teams like all the economy's got to a point where it had to be based on growth. it could not just be sustainable. it had to grow. and that meant more consumers. so, then, that led to a lot of things ecologically that were not good for the earth's, things that people did to maximize profits. so, that is one thing.

5:05 pm

is there the possibility there might be a new economy that is not based on growth? second, if you do not have consumer demand at the same level that he used to -- and of course, i think that is why. one of the pieces that you talked about is that americans are credible consumers come away more than europeans. i went to a store today, and there is so much junk americans will buy and other economies will not. what if consumer demand has changed? and the third thing is, in my own work i deal with a lot people that are getting divorced and not paying their mortgages. for the first time in seeing people say, we just won't pay our mortgage. and that would be unthinkable. previously people would do anything to save their home and their credit. now people do not care. all the time. they say, we just won't pay our mortgage, and they do. so, i think the consumer attitudes about consumption and debt are really different as a

5:06 pm

result of this crisis. i do not know of any of that means anything. >> do we have a couple of hours? it is very important to draw a distinction most economists do not draw. or have not been drawing for a very long time. this has been a calamity for the planet earth. the distinction between growth and development. is one thing to say we want development and another thing to say we what growth. growth is often at the expense of development. so, do not believe in growth of co2 or poison or toxic derivatives. i think we should have a serious recession in these markets, these sectors. but i do believe in education.

5:07 pm

i believe we should invest in our education systems. smaller classes. no high-capacity schools, because they produce morons. the great and the good want their kids to have the best. you mentioned something that i disagree with. the reason why american consumers consume more than europeans is not a cause of some kind of fundamental cultural difference. what you have -- first, america was the only country that had been effectively untouched by the war. so you had more consumption for durables. i am not sure that americans -- naturally, americans would be the first to enjoy them. then, after that, what you have is a massive reduction in the

5:08 pm

real wage, the real median wage. i do not know if you know that. today we do not have a real median wage that is anywhere near where it was in 1972. what has been the effect between 1970's and 2008 is that living standards were being pushed into the ground, hours were being expanded to make ends meet. real hourly wages were declining. they were working longer hours. that put enormous strain on families. my friends in sociology say that this is correlated with a very fast rise in divorce rates in united states. you have the attempt to substitute the loss of quality with quantity.

5:09 pm

the walmart phenomena and. that is why i mentioned the pickles. who gives a damn about one gallon of pickles? it is there. i have a psychoanalytic view of that. a person who feels exploited and works for nothing and has to work much longer hours goes into walmart, buys the jar and feels like he has been able to steal someone's labor. and that is very alienating. this kind of consumerism, which destroys the environment, which creates circumstances of the devolution of living standards -- this is the result of the global surplus recycling, which is why this squeezing of the

5:10 pm

delights of the workers to keep prices low, but to keep the price is lower than germany or japan, to keep the capital coming here, to keep the german and japanese finance going. i don't believe in pointing fingers at anyone. we are all part of this system that we have created over the last few decades. which met its nemesis because of its hubris. >> i would like to ask three questions. one is to summarise, briefly, what did happen in greece? why did we slide further down in the world? number two, could you please summarize an alternative approach? what could, for example, the

5:11 pm

greek prime minister have done instead of what they did it? and third, there is a hamiltonian economic system from 1789 that created a great america before america became a global power -- could that help greece? >> i will answer your questions starting at the beginning. what happened in greece? we created the eurozone. let me put it this way. in our country, because you come from greece, too, they have been monopolizing the headlines. there is something wrong with the world, if this can happen. imagine if there was a fiscal crisis in the great state of delaware that could bring the united states down. i think you would agree if i were to suggest to you there

5:12 pm

was something wrong not with the state of delaware, but with the united states of america. if one state can monopolize the headlines for so long -- it is an indication there's something wrong with the world, right? it is like saying, oh, this snowflake cause the avalanche. this snowflake is to blame. even if you remove the snowflake. the avalanche would have happened. greece has always flirted with debt implosions. we have defaulted a number times over the last century. done it again last march. if it were not part of the eurozone, it would not have been in the headlines. it would be growing back again now. with all its malignancies and corruption, all the rubbish in our country. it has not been enough to stop the recovery from happened.

5:13 pm

we have done this before. we did it in the 1970's, the 1960's, the 1930's. when you lock yourself into a kind of gold standard -- let me or you a little bit with a history on the eurozone and the euro crisis. this is inimately connected with the story i have been telling today. when the global minotaur was happening, america was single- handedly responsible for generating enough demand for germany, to be the exporter, to not have to worry about who was creating demand for the equipment. germany was the net exporter within the eurozone and without

5:14 pm

the eurozone. and so it happened that the eurozone could keep sailing like a beautiful river boat. but with the storm of 2008, they started sinking. and the top people yelled at people that were below decks, saying, why are you allowing the water to sink in? we are going to punish you, and waterboard you fiscally. this is what is happening to greece now. is being fiscally water boarded. it is complete madness. not having learned the lessons of the 1930's, we are repeating all the problems with the gold standard. now, what could the greek government have done? two greek prime ministers. one from 2004 to 2009. in greece, greece has had experience with that since 1974 after the expiration of

5:15 pm

parliamentary democracy. government, regardless of which party is in government, the accelerator to create some kind of flimsy growth, at some point it became clear that we had a cliff. our debt situation would get too much. and then we would hit the brakes. austerity. which creates increased unemployment. but nevertheless, the debt was manageable. they did this up until 2004. 2004 was accelerated because of the olympics. the next government should have stopped it. but unfortunately government is government. government kept the foot firmly on the accelerator. why? because german capital was flowing to the country at cheap rates, financing ponzi schemes.

5:16 pm

it is just like the subprime market here where people were coerced to take loans that could not afford. similarly in greece. so, you had executives coming to greece, bribing politicians. the greek government -- they did not listen. then 2008. the conservative prime minister, he is not a stupid man. he was a terrible prime minister, but he is not a stupid man. you know what he did? he bailed out. he has not spoken since. he affectively called for a general election. he did not contest it. it was much worse than obama's first debate. he appeared before them and was like "don't vote for me." he lost that election. he did not have to call for that election. he called for it to lose it, to

5:17 pm

stay at home. he has not spoken since. he is having a nice holiday. and then there was papandreou. i was an advisor up until 2006. so i am not to blame. who unfortunately, he did not see the crisis of the eurozone collapsing. the eurozone had no foundation. there was an earthquake. it starts unraveling with greece. now, let's say between 1995 and 2008 god and his angels descended on an athens and ran the show. with rationality, omniscience, ethos, and morality. greece would not have been the first domino to fall. but it would have been the third.

5:18 pm

grace would have fallen after ireland or possibly after portugal. it was never designed to sustain a crisis like 2008. we were doomed. finally, the united states that we know today is the result of the crisis of the 19th century and the early 20th century. 1 very preciously saw the crisis -- and still there is a commonality of debt, and effective recycling of debt, the road be no such thing as a nation that was sustainable. you had a crisis that led to a gradual, discreet, fundamental change from the pacific to the atlantic.

5:19 pm

many europeans, like you would imagine or hope, but this crisis in europe would also mean continental consolidation. i do not see that happening, for reasons i will not bore you with. it would be nice to have a united states of europe. >> i have a couple of questions and comment. what do you see in terms of inflation or deflation? my guess would be deflationary. for the average personal investor, what would you advise? my take is treasury-protected securities are pretty good way to go. [laughter] the last comment is -- but shouldn't crease -- shouldn't greece all its own tax collection?

5:20 pm

>> let me start with the last question before i start giving out financial advisor. [laughter] greece certainly should focus on dealing -- not so much with tax collection, but what i call tax immunity. they have a very cozy system of tax immunity. the tragedy is when you have an economy like greece's going to a tailspin and you have a massive immunization of national income, and the central bank is effectively kaput, you can really improve your tax collection methods because there is no income tax. people just do not make money any more. even the rich do not make money.

5:21 pm

other than the money they have already accumulated through geneva or frankfurt. they are not making money. how can you improve your tax mechanism when there's no income to tax? that is the second question. the first question -- i am not worried about inflation at all. in this country, there is this fixation with quantitative easing. bernanke's attempt to stabilize the american economy. it is a policy that i have encountered ever since i came to this country. mr. bernanke is printing money. he is not printing money. if it were, you could talk about the loss potential, which is different from deflationary. but what exactly is quantitative easing?

5:22 pm

i wish he could print money and give consumers the money they need to buy things and pay down their debt. because that does not it added. it relieves negative equity problems. that is why some people refer to him as helicopter ben. before he became the chairman of the fed, he said it would be a good idea in the middle of the great recession to do that. when he buys mortgage-backed securities from jpmorgan, right? effectively what he does is he creates an audit from which jpmorgan controls to pass these mps's to another bank.

5:23 pm

jpmorgan cannot lend that money to you. the only way he can make this happen with qe is if there is an amazing equilibrium among the bankers, and at the same time, they must feel that as a result of this that interest rates will fall sufficiently for house buyers to order new homes from them, so they can make use of those new loans. that is why it as a result of this coincidence of optimism, it is nowhere to be found in this equilibrium of fear that we are experiencing. the money supply is not

5:24 pm

increasing. but bernanke loves to print money. my criticism of quantitative easing is what he is trying to do is to create a new bubble in mortgage-backed securities. we talk about toxic derivatives. they are not really toxic derivatives. what they are is paper priced at very low prices. he is trying to create a bubble. so, it is not a quantitative easing even. i call it price easing. i am not giving you a price on what to buy. i do not want you to blame me. >> unfortunately, that is all the time we have today. we will be having a sign. thank you for coming today. [applause] [captioning performed by

5:25 pm

national captioning institute] [captions copyright national cable satellite corp. 2012] >> later tonight, more interviews with members of congress. we will start with retiring democrat ben nelson. he served two terms and was part of the so-called gang of 14 that helped negotiate a compromise

5:26 pm

over judicial nominations. about 40 minutes later, interviews with two retiring house members. first, house republican jerry lewis, who chairs the appropriations committee. later, california democrat lynn woolsey on her work in congress. >> there are cynics who say that a party platform is something nobody bothers to read that does not often amount to much. whether it is different this time than it has ever been before, i believe the republican party has a platform that is a banner of bold, unmistakable colors with no pastel shades. >> you see the evolution of reagan as a politician.

5:27 pm

he talks in this speech about hope and about the future, and about an america free of having nuclear weapons aimed at them. it is a more optimistic view of the world, not just a denunciation of big government. his anti-communism is evolving. his cultural view is evolving. he has not yet acquired the tax cut philosophy that it so nicely into his outlook of empowered individuals. >> crucially on the political campaigns of ronald reagan, part of four days of american history tv. >> according to a recent pro public a report, parents are

5:28 pm

being saddled with student loans they cannot afford to repay. the national consumer law attorney took part in the discussion examining student loan debt and its effects on both the student and the parents. this is about an hour and 20 minutes. >> with a degree come student debt. i'm really happy to be here tonight. it is great to take some time, to have this many and this whole set up to discuss these things, and these issues. i think propublica does a

5:29 pm

fantastic job with this, as they do with everything. we are happy to have a fantastic panel with the array of experts you would want to be discussing this issue. marion has been covering this for propublica, and a month ago had a fantastic piece that would-be the result of months of investigation of the debt burden on parents. that is an aspect that not a lot of people have been talking about. although you may have read about it on the cover of the "new york times" today, a month ago is when she began talking about it. we have the publisher and author of a best seller called "secrets to winning a scholarship." next to him, an attorney with the national consumer law center and the author of several

5:30 pm

publications including "student loan lot," and "the guide to surviving student debt." next to her is the n.y.u. chief enrollment officer. he is in charge of the office of financial aid. so, to get into the solutions oriented discussion we're going to have today, the problem is something i think everybody is very familiar with, but i think of the saleogle's is an interesting harbinger. if you type in student loan, it will suggest student loan forgiveness. if you type in student debt, it will suggest student debt crisis. this is a problem many people worry about, whether it is at

5:31 pm

3:00 a.m. when they cannot sleep or in the hospital staring at their new baby and wondering, how will i do this the way i want to, the way maybe my parents were able to manage in a previous generation. the average student graduates with $26,600 worth of debt and over 13% default within three years. we have more outstanding student at than auto or credit-card debt at this point. many may think it is good that we have more student debt than credit-card debt, but not if we are not able to pay it back. the current job market and the great recession have made it much worse. i want to have man talk about -- maryann talk about her incredible investigative work

5:32 pm

into how this affects parents. first of all, what are the biggest concerns without population about this dead, and what are the potential solutions for the -- debt, and what are the potential solutions for the parent's side? >> we chose to start with the parents because the federal loan program for parents to borrow through to pay for their children's education. people say that federal loans have card caps of $5,000-$7,000 per year. you can only borrow a total of $33,000 for undergrad. but that is not looking at the parent portion of the picture. the parent portion allows you to borrow as much as you need, to

5:33 pm

fill the annette need, to pay your child's way to get to a -- and meant to need, to pay your child's way to get to a -- unmet need, to pay your child's way to get to a particular school. there is a credit check that is very modest and there is not a check on income. but as costs have grown, perhaps the limits we have had on federal student loans do not meet the needs the students and families are experiencing when they are trying to pay for college. you see the growth in the program where more parents are borrowing from this program. recipients have doubled in the past decade, and they are borrowing more money as well. we thought it was emblematic of the shift in the system. >> would you say the apparent

5:34 pm

lack of paycheck is one of the most consistent missing pieces? if someone has an income of $10,000 a year, they can take out a loan for $30,000. >> if they do not have a negative credit history, and we could have a larger conversation about how fat is defined -- how that is defined, you could come yes, in theory, are much more than you make in the year. >> -- are a much more dna in a year. >> -- borrow much moer thtn you make in a year.

5:35 pm

>> mark, why do think people are taking on so much more debt than they can handle? >> the burden of paying for college has shifted from the federal and state governments to the families. the only type of financial aid that has elasticity is the loans. stafford loans have limits. parent + loans have no aggregate limit. it has nothing to do with the family's ability to repay the debt. the second aspect is the students and parents are chasing the dream, and they will sign whatever piece of paper is put in front of them without paying attention to the details. they figure they will figure out how to deal with it after they graduate. there are ways to reduce your debt such as attending and in state public college or a

5:36 pm

college with generous financial aid policies. that is one of the most effective ways to do that. once you're on campus, you can buy cheaper textbooks and sell them back to the bookstore. but that does not do as much as just going to a less expensive college. >> is the chasing the dream aspect something that in previous generations was possible and able to figure out after work, or is it in knowledge gap in terms of things have changed? why is it more of a problem now, or is it not? >> the debt has grown. when you have a failure of grants to keep pace with the college costs, there are three main ways families deal with it. one is to attend a lower cost college.

5:37 pm

one is to not go to college. the third is to graduate with more debt. we see this manifesting itself first and foremost on lower income students. even though college enrollment as a whole has increased, there has been a shift in undergraduate enrollment among low-income students from bachelor degrees to certificate degrees. a good rule of thumb is that your debt at graduation should be less than your annual starting salary. if it is, you will be able to pay it back in 10 years. more and more families are graduating with an affordable that. given that they do not have an awareness of what it means to take on this debt, and no one is teaching them financial literacy

5:38 pm

in high school or college, smart bar wing is something they are not able to do -- borrowing is something they are not able to do. someone who is getting a bachelor of science in nursing can afford to take on more debt than someone getting a degree in religious studies or a low income field. it does not mean you should abandon the degree. it means you should pay attention to the debt, because you may abandon the dream later. >> not all the trees are worth as much is something those of us -- all degrees are worth as much is something those of us who love liberal arts in the united states have a hard time coming to grips with. >> or journalism. >> is -- it obviously makes

5:39 pm

people uncomfortable that the situation is further curtailed by the family were born into. if you are a wonderful high school student, you have to think more about your major and your college than a student born into a wealthy family. how do you balance that with the reality of this crisis. >> one of the things we do at the national consumer law center is direct representation of low- income borrowers as well as speak to thousands of borrowers throughout the country. we do see the effect of this

5:40 pm

threw out the country. many students do not graduate. there is default. when you think of who alone are worth is -- who the loan borrower is, the majority fall into nontraditional student categories, meaning 25 or older, often financially independent, often have their own families, so just to have that in mind. the problems of four year traditional students are important, but i think they get disproportionate attention. i have clients in their 30's, in their eighties and in their nineties as well. this is a problem that lasts a lifetime. one thing to sort of answer the

5:41 pm

question, a lot of this depends on what we think the goals are of our federal aid policy. i think that is something we can debate a little bit, because historically, the main goals of the aid policies were about social mobility, equal access not just to get into college, but to complete and hopefully succeed financially and help with social mobility issues. looking at that goal, our policies have been a failure. the social mobility part of higher education has not changed much in terms of what family you are born into and what your odds are of going to college.

5:42 pm

one solution i throw out is that i do not think we should be limiting opportunity at the front and so much. i think people when they make decisions are not just chasing a dream. this dream is sold to us from the beginning. college credentials to impact your income. we all make decisions with an optimism bias. we think we are the one that will succeed. the problem for my clients is not that they make worst decisions, it is that the consequences of their decisions is so much worse. it is not the level of debt.

5:43 pm

it could be a small debt that spirals for a client. we should not leave people out to see who is going to succeed. we should not hammered people so much if they get into a little bit of trouble. we do not give people relief. we go after them forever. let's give people the opportunity to go back to school again. that is good for taxpayers too because they're more likely to repay their loans. >> and liu is used as an example in many of these -- and why you is used as an example in many of the stork -- nyu is used as an example in many of these

5:44 pm

stories because it is a sought after school. you say you are uncomfortable with the parent plus program, but you rely on it like other schools. how has nyu been developing policies both from the admissions standpoint and to help students once they get there and end up in trouble? >> first, a little context. and there will answer your question. -- i will answer your question. i do not want to sound like the person who will push this under the rug and a student that is ok, -- it is okay -- student debt is ok, but context is

5:45 pm

important. the disparity is huge as you look across this issue. we talk about a 13% default rate. it varies from 1% at some institution to 40% at others. it is a broad set of issues. i still described as a crisis. what is our definition of a crisis? i am not going to answer that. i think the context of a crisis, and the dilemma is, how do we find the talented student -- and just so you know, i am a farm boy who has worked at four different institutions with very different missions and six different university presidents. i'm a lucky person as well.

5:46 pm

i have seen a broad array of university missions, types of students, profiles of students, and this is an issue across all students, but i do not think it is fair to compare credit-card debt and student loan debt. student loan debt is an investment in the future. there is a payoff, but not to the degree that it puts families and students in a position that will have a significant negative impact on the decisions they make post-graduation. that is kind of the dilemma, but i think it needs to be framed differently than it typically is. it is the crisis component.

5:47 pm

everyone has debt over $100,000. that is not true. if you have ever heard john sexton speak, he will say our financial aid is not what we would like it to be. but even at nyu, the percentage of students with that over $100,000 is very small. i do think context is important. that is where i will start. there is huge disparity across different types of institutions. what we have been doing is a number of things. i have been at nyu about 3 1/2 years. we have affected quite a bit of change in that time. john sexton is completely committed to the following. our goal is to inform families right up front, shop around.

5:48 pm

nyu is a unique place. our value proposition is different than every other institution in the country. we have a global network of campuses. we are in -- i am biased, but the greatest city. we are in greenwich village. we have a world-class faculty. i believe there is a value proposition that is different than other institutions. we are a fabulous place, but we are not the only fabulous place. our message to students from prospect on is about what are you looking for in an institution, what are you looking for in a program? and remember, about half the freshmen who begin this fall will change their major at least once. what are you looking for in a

5:49 pm

program? small, large, internship opportunities, faculty? one thing to consider should be the financial investment, not just the first year, but across four or five years. families will cobble together a package, a financial package, that will get through the first year, and then they find themselves in real difficulty. our goal is not to scare people away, and not to be the latest. we are working hard to get the limited amount of financial aid we have to the right students. we're completely need based. i could count on one hand the number of merit scholarships that are not need based. we are telling families, consider these factors. do not ignore the financial investment. i meet with a lot of families,

5:50 pm

and they are wonderful people, but the first thing they say to me is i have wanted to come to nyu since i was four. what could you really know about the university when you are four? you might know that you like new york city or that alec baldwin came here. but it is important to consider the financial aspect. >> is that something you are stressing more now than you were a few years ago? >> it is. there were families coming to nyu that did not have the financial resources to be there, and we were not in a position to provide the resources to allow them to stay. i do not want to sound like we are an elitist institution

5:51 pm

telling poor kids not to come, but for families thinking about the future, you have to think about the impact this will have in the long term. the other aspect is examining how we invest the budget we have. that is my responsibility. we have made some major changes in how we are awarding financial aid and how we are assessing the financial resources of families. that has been a gain changer for us. we have fundamentally changed how we are awarding lower and middle-income families financial aid. >> you were saying the college debt is good compared to credit card debt.

5:52 pm

>> with a qualifier, but yes. >> the major qualifier for that would be that you graduate, that you end up with a degree, that the college that is not a cliff completing.d oup especially non-traditional students, some are in the single digits after six years. what is the responsibility of the school to help people get to a degree? i know at a place like nyu, do you expect lots of transfer students, for instance, so that people could do community

5:53 pm

college and then graduate with an nyu degree? i do not know if any of you have opinions on getting students to graduation whom -- and who is there to pick up the pieces when things go wrong in the process. >> i can just say that one thing is -- there is actually surprisingly little research on why people default. we did a study this summer which had a very small survey sample, but is shockingly one of the few where it surveyed people who were talked into borrowing and .sked them what thappened

5:54 pm

completing is not necessarily going to lead to success. there are some factors, largely in the for-profit sector to some extent, where completion does not lead to financial success necessarily, but in general, completion is important. there are a number of ways across the board that we can do a better job at this. there are some federal and state government requirements to have more information out there about completion rates and other information about schools. information alone, disclosures alone, in my opinion, are never enough of a consumer protection policy, but they are certainly helpful to some extent. having a consistent way to measure completion is important too.

5:55 pm

people being able to compare apples to apples is important. two different outcome measures is important. many of you may know that the obama administration tried to start doing that, mostly in the for-profit sector, but not exclusively, and has had a lot of opposition over that. i think we will see more efforts coming in the next four years. ise last thing i would say thi what i said earlier, which is that for people who do not complete, knowing that this is a factor that leads to default, that we do not make that the

5:56 pm

final sentence for everybody. let's make it easier for people to transition out of default, to prevent them from getting into default in the first place. the best way to solve the problem is to help people and of succeeding. if you have better completion rates, you have your people in the problem in the first place. >> the key is getting the student who starts to the finish line. the focus on completion rates has a new ones to it. one of the easiest ways for college to have good completion rates is to deny admission to

5:57 pm

high risk students. we need to remove the obstacles that keep students from completing their education. i do not think community colleges are the solution. community colleges are great if you are seeking an associate's degree. but of those who starred at a two-year institution, 20% graduate with a bachelor's degree from an institution where you go for years. two-thirds who starred at the four-year institution finish there. to the extent they are relying

5:58 pm

on debt to make college more affordable, they need the evidence to back it up. if the students were to hear that two-thirds of the students from this college or going to graduate or drop out with more debt than they can afford to pay, they might walk to a college that is less problematic on equal measure. but what is needed is not just federal disclosure of affordability. the financial aid shopping she et is a step in the right direction, but better disclosures are not enough when students and their parents do not have the skills to interpret these disposals. -- these disclosures. a better financial literacy needs to be taught in the secondary school curriculum. it is not as to the making smarter borrowing decisions, it

5:59 pm

is also about helping them be more successful. it is a guide to being a grown- up so the know how to save -- so that you know how to save for a house, prepare for children, save for retirement, save for your children's education. nobody teaches them that and they need to know that so they can make informed decisions. they need those skills. >> i was just going to add that i do think at the department of education level they are trying to push the consumer information angle and to have colleges have those tough conversations without the department having to come down and actually put a hard income limit on something like a parent plus loan. they want that to happen on the

6:00 pm

counseling of all -- level. when i talk to financial aided minister raiders, they are conflicted. who am i? is it my schools place to say that this is too much money to borrow? >> i would be happy to speak to that. there was an article right after that expressed that specifically. counselors are not financial advisers. we do not know what the financial resources are. we know that they have additional information out there. it is our policy that we are not doing any financial adviser in. this is a loan, you have to repay loans.

6:01 pm

we are not qualified, nor should we be making decisions for families and telling them that you can't come here because you can't afford to be here. we don't know what additional resources they might have. i have had conversations with families where you need to consider carefully what this is going to mean long term. you need to have talks that will not result in a kind of that you're going have. short of saying not to come here, they need to think carefully about where they're going to be. let's talk about completion. my background is psychometrics and statistics.

6:02 pm

i understand standardized testing. we make decisions in the more selective institutions based on a set of characteristics. but we are not perfect at it and there are students that we got, the students that succeed at nyu and they're going to other wonderful colleges. i have worked with the school district, a guidance counselor has 600 students assigned to her. they are not getting any really good school counseling. should they not have an opportunity to attend college? for many of those students, their first opportunity to see whether or not they are capable of doing college level work is if they enroll in a community college. if they are not able to do the

6:03 pm

work and they are borrowing, they are saddled with loans that. i am glad that mark mentioned secondary schools. there are huge issues in large school districts, especially, related to family is getting good information, and that out -- is critical solving a lot of these issues. it is not a snap your fingers kind of solution. they're very strapped in terms of resources financial and human. it is broader than retention strategies. how do we start the conversation early enough that families and students understand what the expectations are? it is a broader and more

6:04 pm

complicated mission. >> a perfect segue that i wanted to talk about next, the role of government in all of this, talking about how schools and families and the government can do a better job helping to alleviate this issue for families. one role that the government has is the public-school system. i think the one aspect we have not touched on is the number of students, especially from lower performing districts, and the number of students that graduate and they needed remedial work. they end up using a lot of their loans taking high-school class's, they have gone through and they are already in debt. that is a big issue in new york

6:05 pm

city. that is one huge problem. we also briefly touched on the federal government's role in regulating this whole process and how the push seems to be for disclosure, more information out there will help people be better consumers. the third issue when it comes to the government is the caution that mark issued, the state and the city universities have been defunded over decades, and that as part of the rising tuition costs. a public university level that -- i read once that every time there is a financial crisis, they cut university's first that they never put that back when the economy rebounds.

6:06 pm

we have had tuition rates go way up. in terms of the government, all those different roles that they apply, how much of this is a problem that the private sector and individual families are not as much to blame for. >> there is plenty of blame to go around. we have kindergarten, before kindergarten, and at the college level, someone graduates -- someone who graduates is twice as likely to go on. the debt is having an effect on people's choices, like it or not. a government is responsible for it. there is the failure of grants

6:07 pm

to keep pace with college thoughts. the government is also responsible for the failure of the grants. the other side would like to blame the cost, but i think it is both. those are very interesting aspects. you have students on average having as much, and it is completely skewed towards the funds and it has been -- the way we have a $15,000 program. that would lead to hundreds of thousands of additional bachelor degrees. the grant pays for itself in the decade. that increased federal income tax rate, it pays for the cost

6:08 pm

of the po grant. half of the students are not traditional students, but the half that are, they have a typical work load. yet 10 years to pay back the government for the cost of a grant. then there is a 14% return on investment. it is not as much of an advance from the federal government. we should stop thinking about this as being purely a personal benefit to the students. and there is all sorts of good that comes from higher education. there is a lot of good that stems from a college education

6:09 pm

and as a society, we should be putting the highest possible priority on it. we get what we sow, and you need to be thinking about where we want our society to be in a few decades, and the way to that, and ever improving society is through education, not cutting the one thing that is a real investment. >> another thing i would say, i will give you an example from a parent loan situation. if you get a client, you fail this credit check. you get about $4,000 extra in student loans. i hear this from administrators

6:10 pm

a lot, a lot of people are hoping to get denied that they can get the extra $5,000 because that is what they need to pay their way to an in-state schooler something like that. it is a weird fang, if someone is applying, hoping they can get denied, if that is all they need, should be limits be reconsidered? do they shore up increasing grants? is that something the federal government could or should consider? most of federal student loans, student borrowing is happening through the government, of course. we haven't gotten too much into the private loan conversation which we could, but you have these federal loan services that are handling all of this loan

6:11 pm

revenue. the system is not -- a communication breakdown between the borrowers, servicers and lenders resemble the mortgage market where people fall under hard times and they need a little more flexibility. the amount of paperwork and bureaucracy that stands in a way of relief is something that i think the federal government could and should take a more active role in overseeing >> i spend a lot of my days hanging my head against the wall with the department of education and it has huge costs. administration of the programs themselves is a very important topic.

6:12 pm

getting back to what i said originally, if the goal of federal aid is about social mobility, i think we have to realize that the government policies, they are going to have to be targeted that way. he talked about the need-based aid, it is a way to have hit more targeted. and i think having a conversation about if higher education should be the driver in this country, a lot of people frank, i am not an expert on this that all, the people that are in trouble,-there could be alternatives to college that could lead to some good-paying jobs, a cheapening of the

6:13 pm

credentials, more people have the have college credentials for entry jobs, it impacts lower income individuals as well. that is an important conversation but it is a main driver of mobility. excepting that premise, we should have the targeting go that way. and the 2nd think, again, giving people a break on the back end like i have been talking about is not just about cutting back on some of the draconian policies, but it is what mary and is talking about, making sure the programs of their home actually work. that is the government accountability issue which i think has gotten attention in a very polarized away.

6:14 pm

it is somewhere in between. my experience working with the department of education, for the most part, the tensions are good. it drives people near profit. it is what is right now. and there are benefits of that.

6:15 pm

>> the example of $10,000 of and come and $30,000 of debt, either they are not aware of what that means, for there are expecting the child. i say we get rid of alone and have a rational set of limits on the student loans based on the degree lovell that will specify what the likely in come as going to be. the annual limits of will be proportional. i think that we need to do more on the back end.

6:16 pm

bankruptcy discharge available. we need to restore a statute of limitations. i see many examples in which the loan records are computer printouts and there is no copy of the promissory note. the lender denies it, and records from 30 years ago are often hard to come by. i had a senior citizen approach me that said i could not borrow those loans because i was incarcerated. proving that he doesn't own the loans, he has to, not only under the rules, he has to state that someone else forged the signature, but he has to have

6:17 pm

been caught and prosecuted for him to get one of these false certifications. that is almost impossible to do. we need to attack this from every angle. >> in the province -- in the public good model, the government funded most of it.

6:18 pm

73% of the operating budget came from the state. we have to find other ways to generate revenue. the cost goes up, the price goes up, the subsidy doesn't go up. and we could argue, at what level. i would throw out another model. the comment about setting loan limits based on earning potential makes sense, but we know that students change their

6:19 pm

minds and you could be premed the first semester at a journalism major in your second. >> i started engineering, so i think there has to be some method by which we are limiting loans, but this is not a novel idea. if i were king, which i am not, i would put all of the grant programs and loan programs in one place. it would be in come based repayment. there are all kinds of problems that would need to be worked out. i happened to be in london when they did this model. students were amazingly concerned about the potential outcome. but it is of much more equitable

6:20 pm

model. politically, it is incredibly difficult, but the problem of front is that we don't know, people are actually earning. in a model, there will have to be lots of adjustments made. i think making it loan-based and having them based on income and a set of rules that would keep people from gaming the system is a much better model than trying to plug the hole. and it also addresses the up front issues of students that are, for the first time, able to assess if they are prepared to do college level work. if we base their repayment on their income, if that experience

6:21 pm

doesn't influence their income, they are off the hook. i am not an economist, so i am not -- and in terms of ideas that i see as game changers, that is one that has been flooded and it has worked extremely well and australia and the uk. the political aspect would be huge. >> low-income students are risk averse. they do not have secret bank accounts where they can address the situation. and if they fail, the burdens of being on them. they are less likely to pursue a college education if it means earning more than their parents do in a year. we expect pell grant recipients to graduate with more debt than

6:22 pm

middle and upper income students. they are anywhere from 150% more likely to graduate. we are burdening those the least capable of the most that. the problem is that they are going to impact access. >> the point before you go on, a lot of that is about communicating to families what this means. it is far from perfect, but they are borrowing well beyond their families capability, baking on the fact that they will be able to. i don't disagree that there isn't a perfect model, but i think it has huge potential. >> i want to move on to questions from the audience

6:23 pm

because i want to get in as many as possible. i think what is interesting, so far, there seems to be a lot of changes that would take political will that we don't seem to think necessarily exist right now. a lot of it has to do with education in terms of if the reality is as it is, having people understand it as well as possible which makes tonight so important. in terms of questions from the audience, make sure is a question and not a statement. try to have it be as quick as possible in terms of the phrasing of it. you can direct it to anybody in particular or in general, will try to have the answers be sustained.

6:24 pm

anybody that has questions? >> a couple questions. maybe predators is not the right word, but financial agencies taking a advantage of the availability of two loans, bankruptcy a as i understand it, there is no credit check. then you have the kinsey and sort of lenders. and why you as one thing, but there are other universities. , i if they're selling loans wonder -- [inaudible] and the wonder if a partial answer is early in community colleges, and if an institution like and why you might need to keep it open for people coming

6:25 pm

in that improves their ability. >> we haven't gotten into the issues. we mentioned a for-profit universities. they are getting degrees that are worthless or they are convinced to take got a huge amount of debt. the new york university has been telling people to do their research, and it is an important piece. >> a couple points on the predator peace. if there is one theme throughout my career, it has been some of the creditors in this industry. -- predators in this industry.

6:26 pm

there were a lot of for-profit schools back then that were complete ripoffs, really. that whole industry has evolved to a much more of a publicly funded company 70% of my clients have attended public schools, but people have operating 60%.

6:27 pm

but those are relatively small programs. in the student lending world, we can talk about almost exclusively tonight, there is the issue of accountability that we talked about in the first place. but the lending itself is done by the government and the terms are regulated by the government. there was a very large and thriving in sub-prime market. there is a prime market, also. and similar to the seven prime mortgage area, -- sub-prime mortgage areas, they crashed.

6:28 pm

the third party private student lending market has not bounced back yet. it is kind of responsible for the most part. that is the predatory side of things. it is a really important question. when you look at some of these ways of limiting loans of the government, who is going to come and and fulfill that that -- come in and fulfill that gap? >> the average amount per student increases with increasing college costs. it is much more likely to have 1/3 of your students getting in over their heads. it is going to be the cost of

6:29 pm

college-the grant. there are some good ones, some bad ones, and some very bad ones. i like the rules that the government proposed that have been temporarily suspended by a court case which i expect who ultimately will be resurrected. what is the debt service to income ratio? students are actively repaying their loans. if the college is generating, maybe it should not be eligible. i think those rules should also apply to the non-profit and public areas. it should be every program and

6:30 pm

every college. as long as these rules are well- designed, it will provide real indications of students for what is affordable college education. 95% of students graduate with as much debt as a private non- profit college. not necessarily as good as education, but it's a trigger for the cause. >> i think we are talking about bad actors in the heyday of private student lending markets. we saw a lot of families that were not necessarily going to private colleges. i wrote an article about a

6:31 pm

gardener that sent his son to college. the data may about $21,000 a year, and he was able to borrow six figures for his son. there was no underwriting. and this lender, by the way, the new york attorney general's office, it was the deferred lender list. in some cases, they were accused of paying these schools for preferential treatment. and that was the case with this lender, and you can sort of understand some of the anchor and how it generation of students feel very stuck in some ways, very little relief at this point.

6:32 pm

>> in terms of the transfer students, there was no distinction between the community colleges. they have done rigorous work, they have done well, and we have relationships with community colleges. look to enroll students from the community colleges. >> the majority would be four- year institutions. that is only because of the applicant pool. >> it has been a great job. the question that i heard mentioned before was underwriting, and bankruptcy laws.

6:33 pm

it is a big issue with a lot of people out there. if we say they are allowed to be bankrupt, but we think that is going to affect the current market? we have to cut people off. consider the federal loan program, they will guarantee anybody the ability to repay, but because they know there is a guarantee they'll get the loan paid back. the can't charge them bankruptcy, right? how come we guarantee loans without their ability to pay? and woe schools be interested in standing behind their product? if a student defaults, with the school step up and pay the loan back?

6:34 pm

would they pay that loan back? >> it would as a result of higher tuition because the schools don't necessarily have a substantial endowments. the consequence of bankruptcy discharge would be people in over their head would have the option of the light at the end of the tunnel, it would force the lenders to offer more compromises, since they know that the alternative is losing that loan entirely to a bankruptcy discharge, he might be more willing to offer compromises. and they would increase the fees that they charge. the hit of the lender spread is about 20 or 30 basis points home based on the likely amount of bankruptcy discharge.

6:35 pm

they would still be lending to a lot of people. the average score is around 780 or 790. it is not going to make it that much worse. they are already being lent to a higher-risk individuals. there needs to be some sanity in the system. lending $17,500 which is the aggregate stafford loan to someone getting their certificate or associate's degree. there is no way that individual is going to be able to pay that back. the one that individual to be able to pursue that education, they should be getting that money not in the form of loans. we need to have rational loan limits and you also need to have much more government grant investments in our greatest

6:36 pm

resource, which is our people. >> the student loans can be discharged because of bankruptcy, it is just extremely difficult. but also, when you look at history, looking at what the impact would be, it does not been around for ever. there is not as much study as there probably should be, you can show the pricing did not change that much, there is not a lot of changes made based on bankruptcy calls. in terms of when their behavior, the lenders right now are underwriting more and acting more responsibly because the market crashed and it did not just crash because of some

6:37 pm

random whether event, it crashed because of their irresponsible practices. on the federal government, until 1998, there has been sort of the evolution of bankruptcy policy. there was a time limit, and there is a hard chips system, and this idea that students were running out bear filing for bankruptcy is really not proven either. i think that we can look back at history and i think we need have some relief for the private student loan borrowers. we support restoring bankruptcy rights for federal dollars. >> i believe the protection bureau has floated the idea.

6:38 pm

>> congress should consider, not that congress should. >> he or she said, i think the more important question to ask is why the u.s. relies on student loans at all. >> student loans are cheaper than grants. >> i don't know and which direction he meant this, but the conversation earlier, talking about the public good of education, if they are defunding the state and city institutions and having to provide more

6:39 pm

loans, would that be another solution set you could have a free college experience? >> haunt you just have to have $200 billion to spend on it. where is the money going to come from? families, but only one source that maybe has the kind of money >> is a funding priority. their articles written about this, but health care increases, fuel costs, and prisons have become a much higher priority than education. i am not saying it as a right priority, gosh i think this is

6:40 pm

the heart of the matter. he talked about working at a public university, 73% by the state or whatever and you advance arguments for why education should be funded and, so people actually have a social contract, what do find are effective and what arguments are ineffective? >> i am not sure any of them have been especially effective. it is almost the squeaky wheel of where the dollars have to go. institutions have found a way to generate additional revenue. when i was a freshman, and by

6:41 pm

stafford loan covered room, board, tuition. institutions have been defunded and the cost increase, the grants have not kept pace. it becomes funding priorities based on politics. behind closed doors, i think legislators agree that we should be doing a better job of funding education. but when you have a prison because you have people that you're going to incarcerate, or you can cut the education budget and trust that schools will find a way to make that up, the decision is difficult to find something else. -- fund something else. it is not just higher education,

6:42 pm

it is k-12. >> it was successful in california that instituted increases in taxes for a 20% tuition hike because you can only push people so far. >> beefing part of the problem is the perception, a lot of waste in our education? they would go and profiting some of the educational institutions? >> i think it is sometimes used as a reason, but you can pretty easily show that when you look it increased costs, if we hire people that are deciding, these people, the salary and they expect an increase every year.

6:43 pm

there are some institutions that are less affected than others. i don't hold in why you up as the epitome of efficiency, though we are pretty efficient. we have cut our costs and personnel budget by 20% because we're working really hard to be as efficient as we can be. it doesn't account for or define 73% in a flagship and public university by any means. >> at the end of a recession and for a few years, you have unemployment as a lagging indicator. the states have the have balanced budgets. or there is narrow eligibility. and colleges with main approaches, they raise tuition or shift from in the state

6:44 pm

enrollments to out of state which makes them serve the students of the state less, and it shifts the revenue base for their reduce their enrollments so that if you have a smaller pie, he shrank enrollments. i don't see any magic bullet to fixing this. the argument that it will increase tax revenue is appreciated pillar in it hasn't been successful. no idea has really been successful and the first place the politicians will claim is that the colleges are raising tuition even though it is not their fault. >> or certain degrees of are more needed. there is the example of a nursing degree being fixed and states that have nursing crises,

6:45 pm

the people that want to get the degree cannot provide that because they don't have the money. >> my brother is a director of the nursery program. it is very intense. it is more expensive, even though there is a lot of demand for the graduates. the school has to cut somewhere. >> what influence do those cuts have? it affects quality of instruction, services, the overall quality of the educational experience. when people talk about making cuts, we have to be very concerned about how it affects quality.

6:46 pm

and the other piece to mark's comment is that philanthropy has become a huge component of revenue generation, especially the public coming to this area of very late in the process, so institutions that have $3,000,000,000.4000000953 dollars operating budgets are have a billion and a half dollars to try the subsidize a loss of state funding and it is not enough to make up the difference, but it has been an important part of what institutions are doing as well. instruction,0 >> what do we exps of movement in this area for the second term of president obama? >> i think we still have split control of congress said there is a limit to what he can do on his own. he will try to use the

6:47 pm

regulatory process and executive authority like he daid to do wht he can, but he can't appropriate money. i think there are some things that members of congress will agree with. use the regulatorydisclosure does not c, were very little money, it is likely to be favored by both sides. the reauthorization of the higher education act. it might not happen on time, if we look at the last authorization that was supposed to happen in 2003, they had 13 extension bills. take that long't this time around. there will be a lot of proposals for major changes. then by redesign the student loan programs. they might redesign the grant

6:48 pm

programs. it is worth commenting on >. >> i know that there is certainly aware of it. they have been hearing about this problem, that is one thing that does not require congressional action. the consumer financial protection bureau is the new game in town. people don't think of them as a federal loan side.

6:49 pm

even on the federal side, on the ground, people have already borrowed. having the existing programs work well as incredibly important. >> president obama said a lot on the campaign trail that he wanted to tie federal student and federal aid. we have not seen specifics on that. >> we have seen specifics from a prior version of the proposal.

6:50 pm

for the campus based funding, the perkins loan, the grant, it is the college's success. and keeping the tuition for the price from growing too quickly, the final proposal is somewhat different. president obama did say that he wanted to -- it is exactly the same size as the private student loan market place. it is tied to their keeping tuition increases under control.

6:51 pm

>> there is the possibility of the dream act. i think that it is a big potential. anything else? we have touched on some of this, and there is so much more. at some point, i guess that as far for the future conversation. at least go down a little bit into this incredibly complicated issue. [captioning performed by national captioning institute] [captions copyright national cable satellite corp. 2012]

6:52 pm

>> there are setbacks that say the party politics do not often amount to much. i believe the republican party has a platform that is a banner of bold and unmistakable colors. >> you see the evolution of reagan, and the philosophy as a politician. he talks in this speech about hohhot, -- hope, about nuclear weapons and america free without nuclear weapons. [inaudible] you can see his anti communism is evolving, his culture is evolving.

6:53 pm

it requires the tax cut philosophy and the optimistic outlook for individuals and their own lives. >> craig shirley on the political campaigns of ronald reagan right through new year's day. later tonight, returning members of congress. we sit down with retiring senator ben nelson, part of the gang of 14 that helped negotiate a compromise over judicial -- and interviews with retiring house members. republican jerry lewis.

6:54 pm

and a conversation with lynn woolsey on anti-war work in congress. >> i enjoy that it is straight forward, comprehensive, without a pundit interjecting and that is what i really appreciate. anyone looking to become more familiar with how government works. >> she watches c-span on verizon, created by america's cable companies in 1979, brought to you as a public service by your television provider. a look at the housing market for the next year from today's washington journal. this >> "washington journal" continues. host: lawrence yun is the chief economist and senior vice president for the national

6:55 pm

association of realtors. how would you assess the housing markets today? guest: thanks for inviting me, peter. housing market has turned for the better in 2012. the home sales overall look to be about 10% better this year versus last. home prices on average are up about 5%. in some parts of the country, it's up better than 20%. you are seeing places like las vegas and miami where it's about a 10% gain. there's local market variation, but overall the housing market is recovering. host: if the u.s. government and american taxpayers go over the so called "fiscal cliff" what do you foresee for? the for? guest: the fiscal cliff is going to shave off about 4% of gdp, so that the national economic growth. currently is growing about 2%. you can do very simple mathematics. and we are back in a recession.

6:56 pm

we can anticipate 1 million or 2 million net job losses in 2013. it will be difficult for the housing market to continue its momentum without jobs. so we hope that this cliff can be averted. host: when you look at negotiations going on in washington, does your association have a favorable path towards achieving the fiscal cliff? guest: a $1 trillion budget deficit we have been running annually, that is unsustainable. something needs to be addressed. the shrinking of the time. we have, one has to get something done quickly and then a grand bargain as to get done in the springtime to fundamentally address the long- term budget deficit. but we have to get over the short-term obstacle. we're not looking for any specifics related to whether it

6:57 pm

should be government spending cuts, tax increases, but one thing we are very mindful of is that some politicians have been discussing a mortgage interest deduction as a revenue source. we are opposed to that. 7500 homeowners will be impacted by that. we are aware of that being on the table. host: when you talk of a grand bargain later on, if you are looking at the short term fix and then a grand bargain later on, the mortgage interest deduction could go away. would the realtors fight that deduction? guest: i don't think it will go away. it always comes on the table every decade or so. it's been in place a hundred years. we have to recognize over this time span that 13 u.s. presidents were able to handle the budget to ration without

6:58 pm

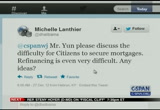

touching the mortgage interest deduction. i think that will also be the case. it's difficult to see an elected official, members of congress going back to their districts to say we are destroying or housing wealth. so i don't think it'll happen. host: there's this article in the wall street journal with charts showing various cities around the u.s. and how well they have done in the last year or so. overall, still down. phoenix, up 21% this year. and this article appeared in yesterday's wall street journal -- what is the realtor association's view on the national governments refinance

6:59 pm

programs they have offered and how do you see expansion of that program? guest: it has worked. this program specifically addressed responsible homeowners. these are homeowners who happen to be under water, yet they have been making their mortgage payments. they may be stuck at 6% or 7% interest rate. the prevailing market interest rate is about 3.5% or 4%. government stepping in to say you have been responsible even in this difficult economic circumstances, if you have to pay your mortgage on time and not defaulted, so let's get you into the current market rate. from the private lenders perspective, they are saying under water, forget it, we will not refinance. for government to step in to help responsible homeowners, it makes perfect sense. host: if you want to dial in to talk with lawrence yun on the 2013 housing market update, the phone numbers are on the screen.

7:00 pm

mr. yun, are any other mortgage housing related issues affected by the fiscal cliff? you talk about the potential of the mortgage tax deduction, but what about on january 1, are there any other tax changes for program changes we should be aware of? guest: the extension of the mortgage forgiveness should be extended. this is referring to people who are under water, they need to sell their house, so they need a short sale approval where the bank would forgive their debt of the underwater amount. from the point of view of the irs, they consider that taxable. so that is people who went through a difficult time and went through a short sale, they went through a very stressful financial times and for the irs

7:01 pm

to say now you have an additional taxable income, does not make sense. we have a bipartisan support to extend this. hopefully we can find a vehicle to attach it to and get it extended. it's only $1 billion price tag. a very small amount compared to the $1 trillion budget deficit we have been running. host: you have been quoted as saying -- with the fiscal cliff we will see 1 million job losses. guest: that is the assessment we have been getting from the running of our models. the economy should be expanding to% or 3% next year without the fiscal cliff, that would correlate with about 2 million net new jobs next year. a it's a continuation of steady expansion. i wish it was a little faster

7:02 pm

expansion, but nonetheless it is an expansion. if we had a fiscal cliff, and we are reversing all the gains we have seen. host: what about mortgage deduction on a second home or vacation home or a certain limit to the size of a mortgage? would you be supportive of that? guest: we have to recognize that negotiating away from what has been a striking departure from just protecting the mortgage interest deduction, property ownership. any breach to that invites further breaches. our members, even though they recognize the deck is a need to be resolved, any breach will lead to further coming back, lowering the income limit. we have to recognize many of the second homes are in places like michigan, wisconsin, arkansas, where people are

7:03 pm

looking for a weekend fishing lodge. it's not the hamptons or very expensive homes in beverly hills. many homes are scattered in the midwest. host: our first call for lawrence yun comes from dan in virginia beach, virginia. caller: i'm interested in this topic, especially being under water, but not terribly under water. some time ago, the president suggested that all the banks or lenders should forgive the difference between where the market is and what they borrowed. i thought, there's not one bank on earth that will do that. here's an idea. i pay $135 a month in my payment for private mortgage insurance. since i have had this home loan, it's over $6,000 that has

7:04 pm

gone through this private mortgage insurance. i thought, if the president wants to do something for me, why not get rid of that. that would lower my payment or increase my payment and that would be a better way to move the housing market forward. i am interested in any comment on that matter. guest: the first think most people would agree on is that market interest rates is 3.5%. to match up the market interest rate will save about $250 per month. a second part is the housing market recovery. we have seen two million people

7:05 pm

that have been under water now above water. we're looking at another two million people that are coming above water. we need to assure that the housing market continues. this is based on the solid factors of supply and demand. this is not the bubble years. those were mistakes that should not have occurred. job creation and affordability. we need to assure the housing market recovers. those are obstacles and we need to make sure they do not occur. host: ron tweets in -- guest: the foreclosure inventory remains large.

7:06 pm

it has been diminishing in the past couple of years. the peak was in 2010. 2011 was lower. we have about 22% of all transactions classified as distressed, either short sells. it had been one third of all transactions a couple of years ago. the distressed property transaction went even further next year, maybe 10% or 15% of all transactions. we are not back to normal by any means. host: we have a tweet from liz smith. guest: the market has recovered.

7:07 pm

the factors that contribute to the recovery helped. the job creation and the bursting out of household formation. this is where many of the adults are living with their parents. that is reducing housing demand. we're seeing many young adults branching out. sometimes they are going into rentals. people do not want to pay higher rents. host: vincent in connecticut. caller: good morning. thank you for appearing. i refinanced this last spring and summer and it was a spectacular success.

7:08 pm

there was a real savings of about $360 a month which is nearly $4,000 a year. with the recent proposals to expand or keep going the program, where is the brunt of the money that is saved? who ends up paying for it? guest: we have to recognize that by getting into the market -- when we have a program that is lowering the rates, their income level is going down. the banking industry was receiving a high interest income and now they are receiving more market competitive income. the profit levels are back to

7:09 pm

pre-recession levels. there is plenty of cash reserve. the current rate is 3.5%. it makes perfect sense. it is good to hear about your specific example of saving $350 per month. host: we have a tweet from bill badey. guest: around 25 million homeowners benefit from that in any particular year. in the early years, they used it and greatly benefited. we've looked at the demographics of it.

7:10 pm

it is primarily younger families. over time, they are paying off their mortgage and they do not use the mortgage interest deduction over time. that is looking at the one side of the accounting ledger. 90% of income taxes are paid by home owners. taking away mortgage interest deduction would mean a higher percentage of taxes would be paid by home owners. host: this is from michele. guest: that is one frustrating aspect. mortgage rates are at historic lows. this is a great time. the time life is much longer.

7:11 pm

the credits core requirement has been ratcheted up. in the past, someone had a credit score of 720, they would be able to get a mortgage. now it requires a score of 760. the housing market was not very normal, people with 720 credit scores would be able to get mortgages. now they are having a tough time. and of the role played by fannie and freddie, pushing it back to the bank. the banks need more clarity about what the rules are so they can be more confident in

7:12 pm

lending. host: what percentage fall into the 760? the max is 800. guest: historically, credit's core of 720 would have qualified. today, 760. how many people are stuck between 720 and 760? today they are being denied. host: is a policy to want looser credit? guest: absolutely not. we need to have a sustainable

7:13 pm

home ownership. wall street was going wild and fannie and freddie were going wild and that led to terrible consequences. when people buy a home, we need to make sure they can stay in their home. the greatest increase in home ownership appeared after the second world war. these were successful home ownerships. some policies -- do not overstretch your budget or you will go into trouble. we had a successful home ownership back then. host: alan, thank you for holding. caller: good morning.

7:14 pm

i have some close friends that are realtors in arizona. they seem to feel some provisions in the dodd-frank bill as far as appraisals go has dampened the real estate market here. they tried to explain it to me. i was wondering if you could explain what those restrictions are on appraisals and what they are meant to do, the benefit. they have some investment properties. they have excellent credit and they cannot seem to refinance those investment properties with any success with that high interest rates. thank you and will listen of the year. guest: appraisal is a friction

7:15 pm

that is present in the current market situation. everything was all set to go. the buyer and seller agreed to a price. someone has to make up for the difference. oftentimes that is a deal breaker. appraisal is a fraction of the marketplace. that is to make the banks become overly conservative as to what the values are. it was needed when the prices were falling. prices now are rising and so the appraisal issue should be diminishing. that should not be troublesome going forward. we hear that appraisals are still a deal breaker. the banks are becoming overly

7:16 pm